Most first-time buyers in Ireland know they need a deposit. What catches people off guard is everything else.

By the time you factor in stamp duty, solicitor fees, a structural survey, mortgage protection insurance, a lender valuation, and the ongoing costs that kick in from day one of ownership, you could easily add €15,000 to €25,000 on top of your deposit. That figure is not a worst-case scenario – for a median-priced Irish home, it is closer to realistic.

This guide covers every cost you will encounter as a first-time buyer in Ireland in 2026: what it is, what it actually costs, and where you can reduce it. The numbers are sourced from Irish lenders, Revenue, Citizens Information, and current market data – not generic estimates copied from a UK equivalent.

We have also updated this for post-Budget 2026 changes, including the extended Help to Buy scheme, the 9% VAT rate on qualifying apartments, and current Central Bank lending rules.

The Context: What You Are Actually Budgeting For

The national median house price in Ireland was approximately €381,000 in late 2025, with Dublin sitting closer to €495,000. These are not asking prices – they are completed sale prices. In competitive areas, properties routinely sell above asking, sometimes 10–20% above what was listed.

The Central Bank rule of thumb that matters most here: first-time buyers can borrow up to four times their gross annual income, with a minimum 10% deposit. Some lenders can offer exceptions – up to 4.75 times income – but these are allocated on a quota basis and are not guaranteed. Plan around the standard limits; treat an exception as a bonus, not a budget strategy.

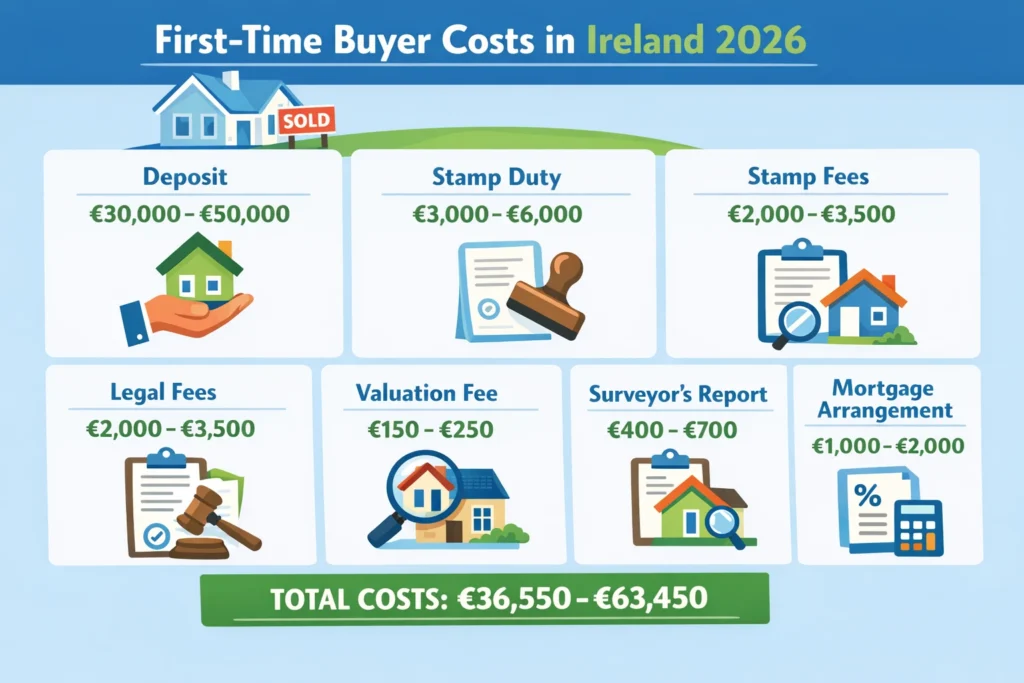

A useful benchmark from experienced mortgage brokers: budget approximately 12% of the purchase price to cover your deposit and all transaction costs combined. That means on a €380,000 property, you should have roughly €45,600 set aside before your mortgage is even drawn down.

Pre-Purchase Costs

The Deposit

First-time buyers must have a minimum 10% deposit. On a €350,000 home, that is €35,000. On a €420,000 home, it is €42,000.

Important: the Help to Buy (HTB) scheme can contribute up to €30,000 or 10% of the purchase price (whichever is lower) towards your deposit – but only for qualifying new-build properties priced at €500,000 or under. If you are buying second-hand, the full deposit must come from your own savings, a gifted deposit from family (accepted by most lenders with documentation), or a combination of both.

The First Home Scheme can bridge a separate funding gap, but it is an equity share arrangement, not a cash contribution to your deposit. These two schemes are distinct and work differently.

Booking Deposit

When you agree to purchase a property, the estate agent will typically ask for a booking deposit to take the property off the market. This is usually between €5,000 and €10,000 for a private sale (sometimes expressed as 2–5% of the purchase price). It is refundable if you choose to walk away before contracts are signed – but once contracts are exchanged, you are legally committed.

This amount is not an additional cost – it comes off your purchase price – but you need it available in cash before mortgage drawdown.

Legal and Tax Costs

Solicitor’s Fees (Conveyancing)

You must appoint a solicitor for the legal transfer of property ownership. This process is called conveyancing, and the fees vary depending on whether you shop around.

Flat-rate conveyancing fees start from around €950 plus VAT (23%) for the most competitive firms. More typically, expect to pay €1,200 to €2,500 plus VAT, depending on the solicitor and property complexity. Some solicitors still quote percentage-based fees – if offered this, ask for a fixed quote instead. The legal work is broadly the same regardless of the house price.

Your solicitor will also handle Land Registry fees on your behalf, which are charged by the Property Registration Authority (PRA) and included in your final legal bill. These vary with the property value but are a relatively modest addition.

Stamp Duty

Stamp duty in 2026 is charged at 1% on the first €1 million of the purchase price, 2% on any amount between €1 million and €1.5 million, and 6% above €1.5 million. For the vast majority of first-time buyers, the 1% rate applies.

One point worth being clear on: Ireland does not offer a stamp duty exemption for first-time buyers. You pay the same rate as everyone else. Some older articles – and occasional estate agent conversations – suggest otherwise. They are wrong. On a €350,000 home, stamp duty is €3,500.

If you are buying a new-build, stamp duty is calculated on the purchase price excluding VAT. VAT on new residential properties is charged at 13.5% and is typically built into the price you pay the developer. From October 2025, qualifying new apartment developments benefit from a reduced 9% VAT rate until 2030 – something that may benefit buyers in cities where apartments make up a larger share of new supply.

Your solicitor will file your stamp duty return with Revenue via the eStamping system and must do so within 44 days of the deed being executed.

Mortgage-Related Costs

Lender Valuation Fee

Before approving your mortgage, your lender will require a professional valuation of the property you intend to buy. This confirms the market value and ensures they are not lending more than the property is worth.

This is not the same as a structural survey. The valuation is carried out by the lender’s own panel valuer, costs between €150 and €300, and is paid by you. It protects the lender, not you.

Structural Survey

A structural survey is separate from the lender’s valuation and is not legally required – but for second-hand homes, it is one of the smartest investments you can make. A qualified chartered surveyor will inspect the property for damp, structural defects, roof condition, subsidence, dry rot, and other issues that would not show up during a viewing.

Survey costs range from around €300 to €800, and more for larger or particularly old properties. For new builds, the concern is reduced but a snagging inspection – where a surveyor walks through before you sign off on completion – is worthwhile at €300 to €500.

Think of a survey as insurance against discovering a €30,000 problem after you have moved in. Walking away from a sale after a survey is financially painful; discovering the problem a year later is significantly more so.

Mortgage Protection Insurance

This is a legal requirement in Ireland if you have a mortgage. Mortgage protection pays off the remaining mortgage balance if you die before the loan is fully repaid. Costs depend on your age, health, the amount you are insuring, and the term of the mortgage.

Typical monthly premiums range from €15 to €50 per person on a joint mortgage. Your lender will require you to have cover in place before drawdown, but you are not obliged to purchase it through your lender – shopping around through a broker often produces cheaper premiums.

Post-Purchase Costs (From Day One of Ownership)

Home Insurance

Lenders require you to have buildings insurance as a condition of the mortgage. This covers the structure of the property – not its contents. Contents insurance is separate and optional, though advisable.

Buildings insurance premiums vary depending on the rebuild value, location, and property type. The Society of Chartered Surveyors Ireland (SCSI) provides a rebuild cost calculator to help you estimate the correct insured amount. Budgeting €400 to €700 per year for a typical home is a reasonable starting point.

Local Property Tax (LPT)

LPT is an annual tax paid to Revenue on all residential properties in Ireland. The amount is based on the property’s market value and falls into valuation bands. For properties valued between €350,000 and €437,500, the annual charge is approximately €450. For properties in the €200,000 to €262,500 band, it is closer to €225. Local authorities have the power to adjust their base rate by up to 15% up or down, so the figure varies slightly by county.

Your solicitor should check for any outstanding LPT liabilities before the sale completes, as they transfer with the property.

Management Fees (Apartments and Multi-Unit Developments)

If you are buying an apartment or a house within a private managed estate, you will pay annual management fees to cover maintenance of shared areas, lifts, car parks, and common facilities. These typically run from €800 to €3,000 per year depending on the development and its amenities. This is an ongoing annual cost, not a one-time purchase expense, and it should factor into your long-term affordability calculation.

Government Schemes That Reduce What You Pay

Help to Buy (HTB)

The Help to Buy scheme is a Revenue incentive that refunds income tax and DIRT paid over the previous four tax years – up to 10% of the purchase price or €30,000, whichever is lower. It applies only to new-build homes or self-builds priced at €500,000 or less.

The scheme has been extended to 31 December 2029. If you qualify for the full €30,000 and your 10% deposit is €35,000, HTB can cover most of that deposit, leaving you to fund the difference from savings. The rebate is paid directly to the developer on your behalf.

One critical detail: both buyers on a joint purchase must be first-time buyers to qualify. If one of you has previously owned a property anywhere in the world, neither of you can use HTB.

First Home Scheme (FHS)

The First Home Scheme is a shared equity initiative where the government and participating banks (currently AIB, Bank of Ireland, and Permanent TSB) buy a stake of up to 30% in your home in return for equity. You do not pay rent on this equity share, but the government holds a proportionate interest in the property.

It is designed for buyers whose mortgage and deposit do not quite reach the purchase price. Unlike HTB, it is not based on income thresholds – eligibility depends on borrowing capacity. You must apply for the maximum mortgage available to you (up to 4 times your income under Central Bank rules).

You can use HTB and FHS together on the same purchase, but the maximum FHS equity available drops from 30% to 20% in that case. And a macro-prudential exception (borrowing above the 4x income limit) disqualifies you from FHS.

A Realistic Budget Example: Buying a €380,000 Home in 2026

| Cost Item | Estimated Amount |

| Deposit (10%) | €38,000 |

| Stamp Duty (1%) | €3,800 |

| Solicitor’s fees (incl. VAT) | €1,800 – €3,000 |

| Land Registry fees | €600 – €800 |

| Lender valuation fee | €150 – €300 |

| Structural survey | €400 – €600 |

| Mortgage protection insurance (annual) | €360 – €1,200 |

| Home insurance (annual) | €400 – €700 |

| Local Property Tax (annual) | ~€450 |

| Moving costs | €500 – €2,000 |

| Booking deposit (deducted from price) | €5,000 – €10,000 |

| TOTAL (beyond purchase price) | ~€8,210 – €12,850 |

Note: The booking deposit is not an additional cost – it is credited against the purchase price at completion. Help to Buy could offset up to €30,000 of the deposit on a qualifying new-build.

Getting This Right Before You Start

The biggest mistake first-time buyers make is fixating on the deposit and treating everything else as a detail to sort out later. In a market where the average Dublin property now costs close to half a million euro and competition from other buyers remains strong, going into the process underprepared carries real risk.

Know your numbers before you get approval in principle. Understand which government schemes apply to your situation – and which do not. And factor in the ongoing costs of ownership, not just the upfront ones.

If you would like a personal breakdown based on your income, savings, and the type of property you are targeting, speaking to a qualified mortgage broker is the most efficient next step. A good broker will not just find you a rate – they will map out your full cost picture and tell you exactly where you stand.